Health Care Law Blog

In May 2026, the Centers for Medicare & Medicaid Services (CMS) implemented a nationwide six-month moratorium on new Medicare enrollments for home health agencies (HHAs) and hospices. The moratorium has raised immediate questions for providers and investors, particularly regarding whether ownership changes or restructuring transactions may be impacted.

1. Scope of the Moratorium

The moratorium, effective May 13, 2026, is aimed primarily at:

- New Medicare enrollment applications for HHAs and hospices; and

- Certain ownership transactions that require a new enrollment ...

Foster Swift attorneys (left to right) Thomas Huyck, Alex Rusek, Jennifer Van Regenmorter, and Badri Yono attended the Institute of Continuing Legal Education's (ICLE) 31st Annual Health Law Institute Seminar in Livonia at Schoolcraft College on Thursday, March 12, 2026.

Co-sponsored by the Health Care Law Section of the State Bar of Michigan, this one-day event covered the latest key updates and critical issues for professionals in the ever-changing landscape of health care law.

Topics included: Current state and federal regulations, investment trends influencing health ...

In recent years, Michigan has been home to two of the largest sexual abuse scandals involving doctors in history: the sexual abuse committed by Larry Nassar while employed by Michigan State University and the sexual abuse committed by Robert Anderson while employed by the University of Michigan. In both circumstances, the former doctors carried out their sexual abuse under the guise of medical procedures and without the informed consent of their targets. Michigan is not alone in being home to these types of sexual abuse scandals as similar acts have been alleged to have been committed by many other health care providers, such as Richard Strauss (Ohio State University), George Tyndall (University of Southern California), Derrick Todd (Bringham and Women’s Faulkner Hospital (Boston, MA)), Major Michael Stockin (United States Army), amongst others.

In recent years, Michigan has been home to two of the largest sexual abuse scandals involving doctors in history: the sexual abuse committed by Larry Nassar while employed by Michigan State University and the sexual abuse committed by Robert Anderson while employed by the University of Michigan. In both circumstances, the former doctors carried out their sexual abuse under the guise of medical procedures and without the informed consent of their targets. Michigan is not alone in being home to these types of sexual abuse scandals as similar acts have been alleged to have been committed by many other health care providers, such as Richard Strauss (Ohio State University), George Tyndall (University of Southern California), Derrick Todd (Bringham and Women’s Faulkner Hospital (Boston, MA)), Major Michael Stockin (United States Army), amongst others.

After the Supreme Court’s ruling in Dobbs v. Jackson Women’s Health Organization overturned Roe v. Wade on June 24, 2022, the Department of Health and Human Services (“HHS”) was tasked with responding to how the Health Insurance Portability and Accountability Act of 1996 (“HIPAA”) would be affected. Particularly, HHS’s Office for Civil Rights has released guidance regarding how the HIPAA Privacy Rule may or may not permit disclosure of an individual’s sexual and reproductive health information without express authorization from the patient.

After the Supreme Court’s ruling in Dobbs v. Jackson Women’s Health Organization overturned Roe v. Wade on June 24, 2022, the Department of Health and Human Services (“HHS”) was tasked with responding to how the Health Insurance Portability and Accountability Act of 1996 (“HIPAA”) would be affected. Particularly, HHS’s Office for Civil Rights has released guidance regarding how the HIPAA Privacy Rule may or may not permit disclosure of an individual’s sexual and reproductive health information without express authorization from the patient.

On April 7, the Centers for Medicare & Medicaid Services (CMS) issued an update to the COVID-19 emergency declaration blanket waivers for specific providers. The memorandum, which was issued by the Director of the Quality, Safety & Oversight Group, details the numerous changes that will take place within 30 or 60 days of the memorandum’s publication.

On April 7, the Centers for Medicare & Medicaid Services (CMS) issued an update to the COVID-19 emergency declaration blanket waivers for specific providers. The memorandum, which was issued by the Director of the Quality, Safety & Oversight Group, details the numerous changes that will take place within 30 or 60 days of the memorandum’s publication.

The Centers for Medicare & Medicaid Services (CMS) have recently released updated guidance regarding hospital co-locations arrangements. After nearly two years of deliberations and revisions, the final Guidance for Hospital Co-location with Other Hospitals or Health Care Facilities (the “Final Guidance”) was released on November 12, 2021 and took effect immediately upon publication. The Final Guidance is meant to address how CMS and other state agency surveyors will evaluate how hospitals share their space, services, and staff.

The Centers for Medicare & Medicaid Services (CMS) have recently released updated guidance regarding hospital co-locations arrangements. After nearly two years of deliberations and revisions, the final Guidance for Hospital Co-location with Other Hospitals or Health Care Facilities (the “Final Guidance”) was released on November 12, 2021 and took effect immediately upon publication. The Final Guidance is meant to address how CMS and other state agency surveyors will evaluate how hospitals share their space, services, and staff.

On December 27, 2021, Governor Gretchen Whitmer signed Senate Bill 759 into law, which took effect immediately. SB 759 allows individuals without a license for the practice of a health profession to perform certain limited duties. For example, students in a health profession training program may perform duties assigned while training.

On December 27, 2021, Governor Gretchen Whitmer signed Senate Bill 759 into law, which took effect immediately. SB 759 allows individuals without a license for the practice of a health profession to perform certain limited duties. For example, students in a health profession training program may perform duties assigned while training.

On July 9, 2021, President Biden issued an Executive Order (EO) on Promoting Competition in the American Economy where he seeks to address many facets of the American economy and promote a more competitive marketplace.

On July 9, 2021, President Biden issued an Executive Order (EO) on Promoting Competition in the American Economy where he seeks to address many facets of the American economy and promote a more competitive marketplace.

On March 2, 2021, the Michigan Department of Health and Human Services (“MDHHS”) issued an Emergency Order that relaxes the visitation requirements for residential care facilities. The December 8, 2020 MDHHS Order involving residential care facilities was rescinded. The March 2, 2021 Order (the “Order”) became effective immediately.

On March 2, 2021, the Michigan Department of Health and Human Services (“MDHHS”) issued an Emergency Order that relaxes the visitation requirements for residential care facilities. The December 8, 2020 MDHHS Order involving residential care facilities was rescinded. The March 2, 2021 Order (the “Order”) became effective immediately.

The U.S. Department of Health and Human Services (“HHS”) recently issued two highly-anticipated final rules (collectively, the “Final Rule”) to modernize and clarify the regulations that interpret the Physician Self-Referral Statute (“Stark”) and the Anti-Kickback Statute (“AKS”). According to HHS, the Final Rule was intended to provide greater flexibility for healthcare providers to participate in value-based arrangements, ease unnecessary compliance burdens, and maintain safeguards to protect patients and Federal healthcare programs from fraud and abuse. The Final Rule will become effective on January 19, 2021.

The U.S. Department of Health and Human Services (“HHS”) recently issued two highly-anticipated final rules (collectively, the “Final Rule”) to modernize and clarify the regulations that interpret the Physician Self-Referral Statute (“Stark”) and the Anti-Kickback Statute (“AKS”). According to HHS, the Final Rule was intended to provide greater flexibility for healthcare providers to participate in value-based arrangements, ease unnecessary compliance burdens, and maintain safeguards to protect patients and Federal healthcare programs from fraud and abuse. The Final Rule will become effective on January 19, 2021.

On October 6, 2020, the Michigan Department of Health and Human Services ("MDHHS") issued an emergency order (the "MDHHS Order") that retains many of the same requirements that apply to residential care facilities under the previously issued executive orders. As noted in a prior blog post, the Michigan Supreme Court recently held that Governor Whitmer did not have authority after April 30, 2020 to issue or renew any executive orders related to the COVID-19 pandemic. Most of the same requirements will continue to apply to residential care facilities under the MDHHS Order. The MDHHS Order became effective immediately, and will remain in effect through October 30, 2020 (and may be renewed through a subsequent order).

On October 6, 2020, the Michigan Department of Health and Human Services ("MDHHS") issued an emergency order (the "MDHHS Order") that retains many of the same requirements that apply to residential care facilities under the previously issued executive orders. As noted in a prior blog post, the Michigan Supreme Court recently held that Governor Whitmer did not have authority after April 30, 2020 to issue or renew any executive orders related to the COVID-19 pandemic. Most of the same requirements will continue to apply to residential care facilities under the MDHHS Order. The MDHHS Order became effective immediately, and will remain in effect through October 30, 2020 (and may be renewed through a subsequent order).

On May 3, 2020, the Michigan Department of Health and Human Services (MDHHS) provided guidance on the best practices for continued compliance with Executive Order 2020-17. Executive Order 2020-17 implemented temporary restrictions on non-essential medical and dental procedures as of March 21, 2020. Executive Order 2020-17 required all hospitals, freestanding surgical outpatient facilities, dental facilities, and state operated outpatient facilities (collectively, “covered facilities”) to temporarily postpone all non-essential medical and dental procedures until the state of emergency in Michigan is lifted. Currently, the state of emergency is set to continue through May 28, 2020 under Executive Order 2020-68.

On May 3, 2020, the Michigan Department of Health and Human Services (MDHHS) provided guidance on the best practices for continued compliance with Executive Order 2020-17. Executive Order 2020-17 implemented temporary restrictions on non-essential medical and dental procedures as of March 21, 2020. Executive Order 2020-17 required all hospitals, freestanding surgical outpatient facilities, dental facilities, and state operated outpatient facilities (collectively, “covered facilities”) to temporarily postpone all non-essential medical and dental procedures until the state of emergency in Michigan is lifted. Currently, the state of emergency is set to continue through May 28, 2020 under Executive Order 2020-68.

On April 23, 2020, the Centers for Medicare and Medicaid Services (CMS) updated its guidance on infection control and prevention of COVID-19 for Home Health Agencies (HHAs). CMS provided initial guidance on March 10, 2020, which addressed the concerns of COVID-19 and provided answers to practical questions impacting HHAs. In this update, CMS has expanded the COVID-19 guidance and regulations to apply to Religious Nonmedical Healthcare Institutions (RNHCIs).

On April 23, 2020, the Centers for Medicare and Medicaid Services (CMS) updated its guidance on infection control and prevention of COVID-19 for Home Health Agencies (HHAs). CMS provided initial guidance on March 10, 2020, which addressed the concerns of COVID-19 and provided answers to practical questions impacting HHAs. In this update, CMS has expanded the COVID-19 guidance and regulations to apply to Religious Nonmedical Healthcare Institutions (RNHCIs).

This blog has since been updated with new information since its original publication. Due to rapidly changing laws and regulations surrounding COVID-19 matters, please consult your attorney and/or advisor for the latest information before taking any action.

On April 15, 2020, Governor Gretchen Whitmer issued Executive Order 2020-50 which provides protection for residents of long-term care facilities and guidance on the reporting, discharge and transfer of COVID-19 patients. Long term care facility residents are particularly susceptible to the rapid spread of COVID-19. The enhanced restrictions and regulations of Executive Order 2020-50 aim to protect both residents and employees of long term care facilities from the virus, while ensuring residents receive the care they need. The restrictions of Executive Order 2020-50 currently continue through May 13, 2020.

This blog has since been updated with new information since its original publication. Due to rapidly changing laws and regulations surrounding COVID-19 matters, please consult your attorney and/or advisor for the latest information before taking any action.

This blog has since been updated with new information since its original publication. Due to rapidly changing laws and regulations surrounding COVID-19 matters, please consult your attorney and/or advisor for the latest information before taking any action.

The Families First Coronavirus Response Act (FFCRA) and the Coronavirus Aid, Relief, and Economic Security Act (CARES) require insurers to cover diagnostic testing for COVID-19 without any cost-sharing or prior authorization requirements. The Trump Administration and Centers for Medicare and Medicaid recognize that financial barriers that deter individuals from receiving testing for COVID-19 must be eliminated, since testing is critical to slowing the spread of the virus.

On April 5, 2020, Governor Whitmer issued Executive Order 2020-37 which extends restrictions on the entry of individuals into health care facilities, residential care facilities, congregate care facilities, and juvenile justice facilities. Previously, Executive Order 2020-07 prohibited visitors that were not necessary to the provision of medical care, to support the activities of daily living, or to exercise the power of attorney or court-appointed guardianship for an individual under the facility’s care from these facilities.

On April 5, 2020, Governor Whitmer issued Executive Order 2020-37 which extends restrictions on the entry of individuals into health care facilities, residential care facilities, congregate care facilities, and juvenile justice facilities. Previously, Executive Order 2020-07 prohibited visitors that were not necessary to the provision of medical care, to support the activities of daily living, or to exercise the power of attorney or court-appointed guardianship for an individual under the facility’s care from these facilities.

Nursing homes are potential hotspots where COVID-19 can quickly spread to vulnerable individuals. Life Care Center in Kirkland, Washington became the epicenter of the outbreak in Washington after the virus spread rapidly among residents. Life Care Center is not the only nursing home affected, as the CDC reported on March 23, 2020 that 147 nursing homes in 27 states have at least one COVID-19 positive patient. Recognizing the need to keep nursing home residents and healthcare workers safe, the Centers for Medicare and Medicaid Services has implemented an enhanced, focused inspection process for nursing homes to combat the spread of COVID-19.

In response to COVID-19, the Centers for Medicare and Medicaid Services has issued blanket waivers of certain requirements so that hospitals and health care systems have the flexibility needed to manage potential surges. The waiver of these requirements is retroactively effective as of March 1, 2020 and lasts until the end of the emergency declaration for COVID-19.

In response to COVID-19, the Centers for Medicare and Medicaid Services has issued blanket waivers of certain requirements so that hospitals and health care systems have the flexibility needed to manage potential surges. The waiver of these requirements is retroactively effective as of March 1, 2020 and lasts until the end of the emergency declaration for COVID-19.

On March 29, Governor Whitmer signed two emergency executive orders in response to the urgent need for help from as many health care professionals as possible in dealing with the COVID-19 pandemic.

On March 29, Governor Whitmer signed two emergency executive orders in response to the urgent need for help from as many health care professionals as possible in dealing with the COVID-19 pandemic.

The Current Context

The Current Context

The novel Coronavirus (“COVID-19”), now classified as a full blown pandemic by the World Health Organization, is projected to continue spreading across Michigan and the United States over the next few months. In less than a month, the global number of confirmed COVID-19 cases has tripled from about 75,000 cases on February 20, 2020, to more than a quarter million cases as of Friday, March 20.

Last year, the Centers for Medicare and Medicaid Services (“CMS”) issued long-anticipated draft guidance concerning shared space and co-location arrangements between hospitals and other providers. The guidance is meant to clarify how CMS and state agency surveyors will evaluate a hospital’s space sharing or contracted staff arrangements when assessing the hospital’s compliance with the Medicare Conditions of Participation (CoPs).

Last year, the Centers for Medicare and Medicaid Services (“CMS”) issued long-anticipated draft guidance concerning shared space and co-location arrangements between hospitals and other providers. The guidance is meant to clarify how CMS and state agency surveyors will evaluate a hospital’s space sharing or contracted staff arrangements when assessing the hospital’s compliance with the Medicare Conditions of Participation (CoPs).

Recently, the Department of Licensing and Regulatory Affairs finalized changes to the licensing rules for Family and Group Child Care Homes and the licensing rules for Child Care Centers. The purpose of these changes is to maintain compliance with the recent amendments to the Child Care Organization Act and the new requirements of the federal Child Care and Development Block Grant.

Recently, the Department of Licensing and Regulatory Affairs finalized changes to the licensing rules for Family and Group Child Care Homes and the licensing rules for Child Care Centers. The purpose of these changes is to maintain compliance with the recent amendments to the Child Care Organization Act and the new requirements of the federal Child Care and Development Block Grant.

On May 28, 2019, the Centers for Medicare & Medicaid Services ("CMS") finalized a rule (the "Final Rule") to update and modernize requirements for the Programs of All-Inclusive Care for the Elderly ("PACE").

On June 21, 2018, the U.S. Department of Labor (“DOL”) issued final regulations that expanded the availability of association health plans ("AHPs"). Those regulations (the "AHP Rules") were summarized in our previous blog article. An AHP is an arrangement that allows small businesses to band together to obtain healthcare coverage as if they were a single large employer.

On June 21, 2018, the U.S. Department of Labor (“DOL”) issued final regulations that expanded the availability of association health plans ("AHPs"). Those regulations (the "AHP Rules") were summarized in our previous blog article. An AHP is an arrangement that allows small businesses to band together to obtain healthcare coverage as if they were a single large employer.

The Centers for Medicare & Medicaid Services ("CMS") recently lifted its temporary moratorium on the Medicare enrollment of new home health agencies ("HHAs"), subunits, and branch locations in Michigan, Florida, Illinois and Texas. As of January 31, 2019, there are no active Medicare provider enrollment moratoria in any state.

The Centers for Medicare & Medicaid Services ("CMS") recently lifted its temporary moratorium on the Medicare enrollment of new home health agencies ("HHAs"), subunits, and branch locations in Michigan, Florida, Illinois and Texas. As of January 31, 2019, there are no active Medicare provider enrollment moratoria in any state.

The Michigan Health Insurance Claims Assessment (“HICA”) tax has been repealed, effective as of October 1, 2018. On June 11, 2018, Governor Snyder signed a series of bills repealing the HICA tax.

The Michigan Health Insurance Claims Assessment (“HICA”) tax has been repealed, effective as of October 1, 2018. On June 11, 2018, Governor Snyder signed a series of bills repealing the HICA tax.

Earlier this year, the Michigan Department of Licensing and Regulatory Affairs (LARA) issued proposed administrative rules relating to the licensing of health care facilities. Currently, there are separate sets of rules that apply to each type of health facility, such as hospitals, hospices, and nursing homes.

Earlier this year, the Michigan Department of Licensing and Regulatory Affairs (LARA) issued proposed administrative rules relating to the licensing of health care facilities. Currently, there are separate sets of rules that apply to each type of health facility, such as hospitals, hospices, and nursing homes.

In response to growing concerns about misuse and abuse of opioid medications, Michigan has enacted three statutes amending the Public Health Code. The new statutes impose specific requirements on physicians, dentists, physician assistants, and nurse practitioners (“prescribers”) who prescribe controlled substances and on pharmacists who fill those prescriptions.

In response to growing concerns about misuse and abuse of opioid medications, Michigan has enacted three statutes amending the Public Health Code. The new statutes impose specific requirements on physicians, dentists, physician assistants, and nurse practitioners (“prescribers”) who prescribe controlled substances and on pharmacists who fill those prescriptions.

Earlier this year, the Internal Revenue Service (IRS) revoked the tax exempt status of an unidentified hospital for failing to comply with the Affordable Care Act (ACA).

Earlier this year, the Internal Revenue Service (IRS) revoked the tax exempt status of an unidentified hospital for failing to comply with the Affordable Care Act (ACA).

Late in the afternoon on March 6, two committees of the U.S. House of Representatives introduced legislation that would replace and repeal significant portions of the Patient Protection and Affordable Care Act, also known as the ACA or Obamacare. The new legislation, titled the American Health Care Act, addresses a number of key complaints that have been raised by employers since the ACA's implementation. Several provisions of the new legislation that are of particular interest to employers are described briefly below.

Late in the afternoon on March 6, two committees of the U.S. House of Representatives introduced legislation that would replace and repeal significant portions of the Patient Protection and Affordable Care Act, also known as the ACA or Obamacare. The new legislation, titled the American Health Care Act, addresses a number of key complaints that have been raised by employers since the ACA's implementation. Several provisions of the new legislation that are of particular interest to employers are described briefly below.

The U.S. Department of Health & Human Services ("HHS") recently issued a final rule that implements the nondiscrimination provisions under Section 1557 of the Affordable Care Act (the "Final Rule"). The Final Rule becomes effective July 18, 2016.

The U.S. Department of Health & Human Services ("HHS") recently issued a final rule that implements the nondiscrimination provisions under Section 1557 of the Affordable Care Act (the "Final Rule"). The Final Rule becomes effective July 18, 2016.

On February 11, 2016, the Centers for Medicare & Medicaid Services (“CMS”) issued its long-awaited Final Rule on Reporting and Returning of Overpayments (the “Final Rule”). The Final Rule, which will become effective on March 14, 2016, implements section 1128J(d) of the Affordable Care Act (“ACA”). This Section of the ACA requires that Medicare providers report and return Medicare overpayments by the later of (A) the date that is 60 days after the date on which the overpayment was identified; or (B) the date any corresponding cost report is due, if applicable (the “60-day rule”). According to CMS, the purpose of the Final Rule is to provide “needed clarity and consistency in the reporting and returning of self-identified overpayments.”

On February 11, 2016, the Centers for Medicare & Medicaid Services (“CMS”) issued its long-awaited Final Rule on Reporting and Returning of Overpayments (the “Final Rule”). The Final Rule, which will become effective on March 14, 2016, implements section 1128J(d) of the Affordable Care Act (“ACA”). This Section of the ACA requires that Medicare providers report and return Medicare overpayments by the later of (A) the date that is 60 days after the date on which the overpayment was identified; or (B) the date any corresponding cost report is due, if applicable (the “60-day rule”). According to CMS, the purpose of the Final Rule is to provide “needed clarity and consistency in the reporting and returning of self-identified overpayments.”

CMS issued a Proposed Rule on Reporting and Returning of Overpayments (the “Proposed Rule”) on February 16, 2012. The Final Rule includes some important changes to the provisions of the Proposed Rule. A summary of the major provisions of the Final Rule appears below.

In the last few days of 2015, the Internal Revenue Service ("IRS") published welcomed relief for employers who are struggling to understand their reporting obligations under the Affordable Care Act ("ACA"): extended deadlines.

In the last few days of 2015, the Internal Revenue Service ("IRS") published welcomed relief for employers who are struggling to understand their reporting obligations under the Affordable Care Act ("ACA"): extended deadlines.

In a first-of-its-kind and closely followed case, a U.S. district court denied a New York health system's (Healthfirst’s) motion to dismiss the U.S. government's and State of New York's complaints in intervention under the federal False Claims Act (FCA) and New York state counterpart. This case represents the first time that the government has intervened in an FCA case based upon an allegation that a party violated the "60 day rule." The 60 day rule came into existence with the passage of the Affordable Care Act (ACA) in 2010 and subjects parties to FCA liability for failing to report and refund an overpayment within 60 days of identification, even if the defendant received the payment through no fault of its own.

The case, Kane ex rel. United States et al. v. Healthfirst et al., involves three hospitals that were part of the Healthfirst health system network and provided care to patients that were part of Healthfirst's Medicaid managed care plan. Healthfirst received payments from the New York State Department of Health (DOH) in return for services provided to Medicaid eligible enrollees.

The government's allegations stem from overpayments to Healthfirst as a result of a software glitch. Healthfirst was first questioned about the possible overpayments by the New York State Comptroller's office in 2010. The health system tasked Kane, an employee and the eventual whistleblower in the case, to look into the payments. Five months later Kane emailed Healthfirst management a spreadsheet listing over 900 claims totaling more than $1 million that contained an erroneous billing code that may have led to the overpayments.

On June 25, 2015, the Supreme Court of the United States issued a ruling related to the Patient Protection and Affordable Care Act (the "Act") in the case of King v Burwell. The issue that the Court addressed was whether tax credits were available to individuals who purchased health insurance coverage through a Health Insurance Exchange ("Exchange") that was established by the Federal government.

An Exchange serves as a marketplace where individuals can compare various health insurance plans and ultimately purchase health insurance coverage. The Act requires an Exchange to be established in each State. If a State fails to establish its own Exchange, the Federal government is required to step in and establish the Exchange for that State. The Court's decision had the potential to preclude tax credits for individuals purchasing insurance through the Federal Exchanges in 34 States, including Michigan.

This issue was of significant importance because of its implications for the Act's Employer Mandate, which generally requires large employers to offer health insurance coverage to their full-time employees. The tax credits provided under the Act serve as the lynchpin for liability under the Employer Mandate. Despite the fact that a large employer may fail to offer health insurance coverage to its full-time employees, it will not be penalized if those employees do not obtain coverage through the Exchange and receive a tax credit. Therefore, large employers located in States that have a Federal Exchange could arguably avoid penalties for their failure to offer coverage to their full-time employees; such employees would not receive a tax credit when purchasing health insurance coverage on the Exchange and would not trigger the penalty.

Rural hospitals across the United States struggling to stay open

According to the National Rural Health Association, approximately 50 hospitals in the rural United States have closed since 2010. The number of annual closures is growing. Congressional healthcare budget cuts and policy changes significantly affect rural hospitals because rural hospitals often have a disproportionate number of patients who are covered under Medicare, Medicaid or who are uninsured. A number of factors affect and pose challenges to rural hospitals. One challenge is the difficulty of attracting talent, which often means paying more to healthcare professionals in order to recruit them for employment at a rural hospital. Other challenges facing rural hospitals include:

- changing demographics;

- advances in medical practice that the hospital may be unable to implement;

- new federal regulations and standards that create additional compliance related pressure; and

- lower reimbursement rates for Medicare and Medicaid.

Closures of rural hospitals may force individuals to travel long distances for medical care, which may lead to an increase in mortality rates. The closures may discourage business ventures in rural areas due to the increased costs associated with not having a healthcare facility nearby. Metropolitan hospital closings have increased recently, but the existence of medical care alternatives in metropolitan areas typically reduces the effects that closures have on patients.

The Affordable Care Act ("ACA") authorizes the innovative payment model referred to as direct primary care, and more commonly known as “concierge medicine.” Under the direct primary care model, patients can access comprehensive coverage of basic healthcare services for a flat monthly fee. Such services generally include guaranteed same-day or next-day visits with no waiting times. Concierge medicine is becoming increasingly popular in states where it is allowed.

The Affordable Care Act ("ACA") authorizes the innovative payment model referred to as direct primary care, and more commonly known as “concierge medicine.” Under the direct primary care model, patients can access comprehensive coverage of basic healthcare services for a flat monthly fee. Such services generally include guaranteed same-day or next-day visits with no waiting times. Concierge medicine is becoming increasingly popular in states where it is allowed.

On February 18, 2015, the Internal Revenue Service (“IRS”) provided further guidance related to the issue of how certain employer health insurance reimbursement arrangements are treated under the Affordable Care Act (“ACA”).

On February 18, 2015, the Internal Revenue Service (“IRS”) provided further guidance related to the issue of how certain employer health insurance reimbursement arrangements are treated under the Affordable Care Act (“ACA”).

As we explained in a previous post, after the Health Insurance Marketplace opened for business, many employers recommended that their employees use it to purchase individual health insurance policies, with the promise that the premium costs would be reimbursed by the employer. In fact, such employee reimbursement strategies were aggressively marketed to employers as a solution to reduce costs and comply with the requirements of the ACA. Little did these employers (and marketers) know, such arrangements exposed the employers to significant penalties under the ACA.

Prior guidance made clear that such arrangements – whether funded on a pre- or post-tax basis – may be subject to the ACA’s market reforms. Employers that offer reimbursement arrangements that violate the ACA are subject to a $100 per day per affected employee penalty.

Notice 2015-17 clarifies previous guidance and provides transition relief to certain small employers from ACA penalties. Key aspects of the new guidance are noted below.

The February issue of the American Health Lawyers Association’s AHLA Connections features a list of the top ten issues that will impact healthcare law in 2015. We summarized the first five topics in a previous blog. (Miss our summary of the first five? Please click here.)

The February issue of the American Health Lawyers Association’s AHLA Connections features a list of the top ten issues that will impact healthcare law in 2015. We summarized the first five topics in a previous blog. (Miss our summary of the first five? Please click here.)

Here are the remaining trends to think about:

The February issue of the American Health Lawyers Association’s AHLA Connections features a top-ten list of the issues that will impact healthcare law in 2015. This two-part series discusses these important trends.

Here are the first five:

Since the approval of the Affordable Care Act in 2010, hospital consolidation has been on the rise and according to a report detailed in a recent Chicago Tribune article, 2014 followed suit with a “flurry of mergers, acquisitions and joint ventures.” The article features findings from a report issued by healthcare consulting firm Kaufman Hall, including that in 2014 95 deals were announced, down slightly from 98 in 2013 but up from 66 in 2010.

Since the approval of the Affordable Care Act in 2010, hospital consolidation has been on the rise and according to a report detailed in a recent Chicago Tribune article, 2014 followed suit with a “flurry of mergers, acquisitions and joint ventures.” The article features findings from a report issued by healthcare consulting firm Kaufman Hall, including that in 2014 95 deals were announced, down slightly from 98 in 2013 but up from 66 in 2010.

Passage of the Affordable Care Act (ACA) in 2010 increased pressure on hospitals to operate more effectively and efficiently, which has driven industry consolidation. The ACA favors a service model that rewards organizations for producing quality outcomes – not quantity – and many providers believe that compliance will be easier with the greater scale and integration enabled by mergers. Through consolidation, many also hope to be better positioned to attract new patients with expanded services and medical specializations.

Additionally, the ACA’s introduction of a massive wave of new patients into the healthcare system, combined with diminishing Medicaid and Medicare reimbursements, means that the business of healthcare is becoming increasingly expensive, especially for independent hospitals. Another challenge – and driving force behind consolidation – has been the need to upgrade IT systems and facilities to comply with rules and regulations beyond the ACA.

Reduced reimbursements. A shift toward global payment. A demand for integration, quality of care and medical specializations. In order to compete amidst today’s healthcare market pressures, independent hospitals in Michigan and around the nation are increasingly deciding that they cannot go it alone. A recent Detroit News article reveals how this trend is playing out in Metro Detroit, with one of the region’s last two independent hospitals poised for acquisition.

Reduced reimbursements. A shift toward global payment. A demand for integration, quality of care and medical specializations. In order to compete amidst today’s healthcare market pressures, independent hospitals in Michigan and around the nation are increasingly deciding that they cannot go it alone. A recent Detroit News article reveals how this trend is playing out in Metro Detroit, with one of the region’s last two independent hospitals poised for acquisition.

Observers of Detroit’s healthcare environment are reportedly not surprised by the news that Crittenton Hospital Medical Center has signed a letter of intent to join St. Louis-based Ascension Health, the largest Catholic and nonprofit health system in the nation. With Monroe-based Mercy Memorial Hospital announcing on January 6 that it is joining the ProMedica health care company, the Crittenton deal will leave Doctors’ Hospital in Pontiac as the region’s last remaining independent hospital.

Laura Wotruba, spokeswoman for the Michigan Health and Hospital Association, said that this is not a Michigan issue, but rather a widespread pattern. “[It is] a national trend [and] something we’ve been seeing around the country.”

Employers, including municipal employers, have historically struggled to develop a health insurance benefit program for their employees that provides quality benefits and is cost-effective. After the Health Insurance Marketplace opened for business, many employers recommended that their employees use it to purchase individual health insurance policies, with the promise that the premium costs would be reimbursed by the employer. In fact, such employee reimbursement strategies were aggressively marketed to employers as a solution to reduce costs and comply with the requirements of the Patient Protection and Affordable Care Act (“ACA”). Little did these employers (and marketers) know, such arrangements exposed the employers to significant penalties under the ACA.

Employers, including municipal employers, have historically struggled to develop a health insurance benefit program for their employees that provides quality benefits and is cost-effective. After the Health Insurance Marketplace opened for business, many employers recommended that their employees use it to purchase individual health insurance policies, with the promise that the premium costs would be reimbursed by the employer. In fact, such employee reimbursement strategies were aggressively marketed to employers as a solution to reduce costs and comply with the requirements of the Patient Protection and Affordable Care Act (“ACA”). Little did these employers (and marketers) know, such arrangements exposed the employers to significant penalties under the ACA.

In September 2013, the IRS issued Notice 2013-54 that made clear that an employer arrangement that paid for employees’ individual health insurance policy premiums on a pre-tax basis violated the ACA. An employer that offered such an arrangement would be subject to a $100 per day per affected employee penalty ($36,500 per year, per employee).

On Nov. 7, the U.S. Supreme Court decided it would hear a case concerning the health insurance subsidies provided to millions of Americans under the Patient Protection and Affordable Care Act. A June 2015 decision is expected in the case of King v. Burwell, which challenges the Internal Revenue Service’s authority to regulate tax-credit subsidies for coverage purchased through health insurance marketplaces established by the federal government (such as the Michigan health insurance marketplace). Nationwide, more than four out of five people who have received coverage through a federal marketplace are getting a tax credit.

On Nov. 7, the U.S. Supreme Court decided it would hear a case concerning the health insurance subsidies provided to millions of Americans under the Patient Protection and Affordable Care Act. A June 2015 decision is expected in the case of King v. Burwell, which challenges the Internal Revenue Service’s authority to regulate tax-credit subsidies for coverage purchased through health insurance marketplaces established by the federal government (such as the Michigan health insurance marketplace). Nationwide, more than four out of five people who have received coverage through a federal marketplace are getting a tax credit.

As is well known by now, transitional relief from the Patient Protection and Affordable Care Act's Employer Mandate in 2015 is available for certain applicable large employers that sponsor non-calendar year health plans. This transitional relief allows the employer to avoid penalties for those months of 2015 that predate the first day of the non-calendar plan year. What is not so well-known, however, are the requirements that must be met in order for the employer to be entitled to receive the transitional relief.

As is well known by now, transitional relief from the Patient Protection and Affordable Care Act's Employer Mandate in 2015 is available for certain applicable large employers that sponsor non-calendar year health plans. This transitional relief allows the employer to avoid penalties for those months of 2015 that predate the first day of the non-calendar plan year. What is not so well-known, however, are the requirements that must be met in order for the employer to be entitled to receive the transitional relief.

The Centers for Medicare & Medicaid Services ("CMS") recently

announced proposed changes to the Medicare home health prospective payment

system (“PPS”) for the 2015 calendar year. CMS is proposing to tighten eligibility

requirements for home health services

and set a minimum requirement on Home Health Agencies ("HHAs") to

prove their effectiveness, as well as revise how much CMS will pay for certain

services. These proposed changes are expected to reduce Medicare payments to

HHAs by $58 million next year alone, a reduction of .30 percent.

To qualify for the Medicare home health benefit, a beneficiary must be under the care of a physician, have a need for skilled nursing care, physical therapy, speech-language pathology, or continued need for occupational therapy. Further, the beneficiary must be homebound and receive home health services from a Medicare approved agency.

The proposed changes include the following:

In a recently released 26 page report the Department of Health and Human Services revealed that federal subsidies cover 76 percent of premiums for those who have signed up for coverage under the Affordable Care Act in the 36 federally administered markets. According to the Los Angeles Times, the total cost of subsidies could exceed $16.5 billion this year, which is significantly higher than the $10 billion cost that the Congressional Budget Office projected earlier this year.

In a recently released 26 page report the Department of Health and Human Services revealed that federal subsidies cover 76 percent of premiums for those who have signed up for coverage under the Affordable Care Act in the 36 federally administered markets. According to the Los Angeles Times, the total cost of subsidies could exceed $16.5 billion this year, which is significantly higher than the $10 billion cost that the Congressional Budget Office projected earlier this year.

The Affordable Care Act, enacted on

March 23, 2010, has established a number of new requirements that nonprofit

hospitals must meet to maintain tax exemptions. Some of these new obligations,

all codified in Section

501(r) of the Internal Revenue Code, include community health needs

assessment and implementation, financial assistance and emergency care policies,

limits on charges, and billing and collection restrictions.

The Affordable Care Act, enacted on

March 23, 2010, has established a number of new requirements that nonprofit

hospitals must meet to maintain tax exemptions. Some of these new obligations,

all codified in Section

501(r) of the Internal Revenue Code, include community health needs

assessment and implementation, financial assistance and emergency care policies,

limits on charges, and billing and collection restrictions.

In June 2012, the IRS released proposed regulations offering guidance to tax-exempt hospitals relating to certain provisions of Section 501(r). Although, the proposed regulations do not have the force of law, hospitals may rely on these to assist in implementing the requirements.

Below is a brief summary that highlights some of the new requirements for tax-exempt hospitals. Please refer to the full rule, Section 501(r) or contact us, to explore the extent of the new requirements in more detail.

Community health needs assessment and implementation (CHNA)

Effective for tax years beginning after March 23, 2012, hospital facilities must conduct a CHNA and adopt an implementation strategy at least once every three years.

Approximately 9 million people in the United States are covered by both Medicare and Medicaid, including seniors with low income and younger people with disabilities. These so-called "dual eligibles" often have complex and costly health needs, and lawmakers have been seeking ways to reduce costs while maintaining and improving care for this segment of the population. Traditionally, coverage and care for dual eligibles has tended to be fragmented and expensive given the challenges posed by separate entities (Medicare and Medicaid) with separate coverage policies.

Approximately 9 million people in the United States are covered by both Medicare and Medicaid, including seniors with low income and younger people with disabilities. These so-called "dual eligibles" often have complex and costly health needs, and lawmakers have been seeking ways to reduce costs while maintaining and improving care for this segment of the population. Traditionally, coverage and care for dual eligibles has tended to be fragmented and expensive given the challenges posed by separate entities (Medicare and Medicaid) with separate coverage policies.

A number of states, including Michigan, have been working with the Centers for Medicare and Medicaid Services (CMS) to develop proposals to address these challenges, based on new authority in the Affordable Care Act. Through this initiative, 15 states were granted federal funding to help them better coordinate care for dual eligibles. Each of the states, including Michigan, was awarded up to $1 million to help develop new strategies and programs addressing these challenges.

The Patient Protection and Affordable Care Act requires that certain health insurance providers pay an annual fee based on the net premiums they wrote during the preceding calendar year. The providers required to pay this fee include health insurance issuers; health maintenance organizations; certain insurance companies; insurers providing Medicare Advantage, Medicare Part D, or Medicaid coverage; and multiple employer welfare arrangements.

The Patient Protection and Affordable Care Act requires that certain health insurance providers pay an annual fee based on the net premiums they wrote during the preceding calendar year. The providers required to pay this fee include health insurance issuers; health maintenance organizations; certain insurance companies; insurers providing Medicare Advantage, Medicare Part D, or Medicaid coverage; and multiple employer welfare arrangements.

In order to calculate the fees, the Internal Revenue Service (“IRS”) must obtain information related to the amount of net premiums written by each health insurance provider. This is accomplished through IRS Form 8963 (Report of Health Insurance Provider Information). Health insurance providers are required to submit Form 8963 to the IRS by April 15 of each year.

On Feb. 12, 2014, the U.S. Department of Treasury and the Internal Revenue Service published final rules (the “Final Rules”) related to the Employer Shared Responsibility provisions of the Patient Protection and Affordable Care Act (“PPACA”). The Employer Shared Responsibility provisions, referred to as the “Employer Mandate,” generally require certain employers to offer minimum essential health care coverage to their full-time employees or face penalties. The Employer Mandate was originally scheduled to become effective on Jan. 1, 2014 but was delayed until Jan. 1, 2015.

On Feb. 12, 2014, the U.S. Department of Treasury and the Internal Revenue Service published final rules (the “Final Rules”) related to the Employer Shared Responsibility provisions of the Patient Protection and Affordable Care Act (“PPACA”). The Employer Shared Responsibility provisions, referred to as the “Employer Mandate,” generally require certain employers to offer minimum essential health care coverage to their full-time employees or face penalties. The Employer Mandate was originally scheduled to become effective on Jan. 1, 2014 but was delayed until Jan. 1, 2015.

The Final Rules include a second delay of the Employer Mandate. They provide that employers who employ 50 – 99 full time equivalent employees will not be required to comply with the Employer Mandate until Jan. 1, 2016. Additionally, those employers who employ 100 or more full time equivalent employees must offer minimum essential coverage to only 70 percent of those full time employees by Jan. 1, 2015 (as opposed to the 95 percent coverage requirement under the previous regulations). Those employers employing 100 or more full time employees will be required to offer coverage to 95 percent of all full time employees by Jan. 1, 2016. The chart below summarizes the basic details concerning this delay.

On Jan. 2, 2014, the Department of Health and Human Services (“HHS”) issued a proposed rule related to the Administrative Simplification requirements of the Health Insurance Portability and Accountability Act of 1996 (“HIPAA”). Specifically, it delayed the date by which health plans must certify compliance with certain operating rules imposed by the Affordable Care Act (“ACA”).

On Jan. 2, 2014, the Department of Health and Human Services (“HHS”) issued a proposed rule related to the Administrative Simplification requirements of the Health Insurance Portability and Accountability Act of 1996 (“HIPAA”). Specifically, it delayed the date by which health plans must certify compliance with certain operating rules imposed by the Affordable Care Act (“ACA”).

The ACA required the Secretary of HHS to adopt operating rules related to claims status, eligibility, electronic funds transfers ("EFT") and health care payment and remittance advice transactions ("ERA"). Health plans (and other covered entities) were required to comply with the claims status and eligibility operating rules by Jan. 1, 2013 and the EFT and ERA operating rules by Jan. 1, 2014. Additionally, health plans were required to file a statement with HHS certifying that the health plan is in compliance with the operating rules. This certification statement was due by Dec. 31, 2013.

While originally scheduled to start in 2014, now beginning in 2015, "large employers" will be required to provide adequate health care coverage to their full time employees or pay a penalty. This requirement is known as health care reform’s Employer Mandate. In order to assess whether your company is subject to the Employer Mandate, you must first determine whether your company is a "large employer."

While originally scheduled to start in 2014, now beginning in 2015, "large employers" will be required to provide adequate health care coverage to their full time employees or pay a penalty. This requirement is known as health care reform’s Employer Mandate. In order to assess whether your company is subject to the Employer Mandate, you must first determine whether your company is a "large employer."

Technical glitches. Partisan rancor. Breathless media coverage. The rollout of the online Health Insurance Marketplaces (also known as Exchanges) did not lack for drama or controversy. The unveiling of the Marketplaces, one of the key elements of the Patient Protection and Affordable Care Act, was perhaps the most anticipated and controversial website launch in history. The website www.healthcare.gov was flooded with traffic from the moment it opened on October 1, 2013 and many interested consumers ran into trouble. While most of the extensive media coverage of the Marketplaces focused on problems nationally, we wanted to take a look at how Michigan’s Marketplace (and consumers) fared.

Technical glitches. Partisan rancor. Breathless media coverage. The rollout of the online Health Insurance Marketplaces (also known as Exchanges) did not lack for drama or controversy. The unveiling of the Marketplaces, one of the key elements of the Patient Protection and Affordable Care Act, was perhaps the most anticipated and controversial website launch in history. The website www.healthcare.gov was flooded with traffic from the moment it opened on October 1, 2013 and many interested consumers ran into trouble. While most of the extensive media coverage of the Marketplaces focused on problems nationally, we wanted to take a look at how Michigan’s Marketplace (and consumers) fared.

An October 1, 2013 deadline is looming for many employers to give employees written notices under the Patient Protection and Affordable Care Act (PPACA, commonly known as the health care reform act.)

The Michigan Medicaid expansion saga has seemingly come to an end, as the Republican-led state Senate narrowly approved Medicaid expansion on Tuesday, August 27 in a 20-18 vote. Eight Republicans joined 12 Democrats to pass a bill that will bring billions of dollars in federal dollars to Michigan to implement a major element of the Patient Protection and Affordable Care Act. Under this bill, approximately 400,000 additional Michigan residents will be eligible for Medicaid coverage.

The Michigan Medicaid expansion saga has seemingly come to an end, as the Republican-led state Senate narrowly approved Medicaid expansion on Tuesday, August 27 in a 20-18 vote. Eight Republicans joined 12 Democrats to pass a bill that will bring billions of dollars in federal dollars to Michigan to implement a major element of the Patient Protection and Affordable Care Act. Under this bill, approximately 400,000 additional Michigan residents will be eligible for Medicaid coverage.

The vote came after lengthy debate in the Senate on the measure, and passed after "eleventh hour" legislative maneuvering. The Michigan House, which previously passed a Medicaid expansion bill, will likely approve the Senate version of the bill next week. If passed, it will be sent to Governor Snyder's desk for his signature.

In early July, we updated our readers regarding the status of the Medicaid expansion debate in Michigan. At that time, a House-passed bill - supported by Governor Snyder - languished in a Senate committee because it was blocked by Senate Republicans who opposed the measure.

So far, July has been a busy month for health care fraud enforcement across the country.

So far, July has been a busy month for health care fraud enforcement across the country.

On July 18, Divyesh Patel, owner of Alpine Nursing Care Inc. in North Randall, Ohio, was sentenced to two years in prison after pleading guilty to one count of conspiracy to commit health care fraud and four counts of health care fraud. Patel was also ordered to pay total restitution of $1,939,864 to the Medicaid Program in Ohio. According to court documents, Patel hired Belita Mable Bush as the office manager despite knowing that Bush had been convicted of a health care-related felony and excluded from involvement in billing federal health care programs. From June 1, 2006 to October 18, 2009, Patel conspired with Bush to defraud Medicaid by billing for services that had never been performed or that had been performed by excluded individuals. The conspiracy resulted in losses of approximately $1.9 million to the Medicare and Medicaid programs. Bush was convicted on similar charges and will be sentenced next month.

According to a recent Modern Healthcare article, up to 9 of the 32 Pioneer Accountable Care Organizations ("ACOs") may be leaving the program. Four have already notified providers of such withdrawal. Of the 9, 4 of the departing ACOs tentatively say they will be joining Medicare's lower- risk ACO alternative – the Medicare shared savings program. The deadline for deciding whether or not to remain in the Pioneer program is July 31, 2013.

According to a recent Modern Healthcare article, up to 9 of the 32 Pioneer Accountable Care Organizations ("ACOs") may be leaving the program. Four have already notified providers of such withdrawal. Of the 9, 4 of the departing ACOs tentatively say they will be joining Medicare's lower- risk ACO alternative – the Medicare shared savings program. The deadline for deciding whether or not to remain in the Pioneer program is July 31, 2013.

On July 2, 2013, the Obama administration declared that it was delaying the effective date of the Patient Protection and Affordable Care Act’s Employer Mandate until January 1, 2015. The Employer Mandate, which was scheduled to become effective on January 1, 2014, required all large employers to offer health care coverage to their full-time employees or pay a penalty. Most importantly, this delay means that the penalties to large employers for failure to provide health insurance coverage will not be enforced for another year. You may read the full statement issued by the U.S. Department of Treasury here.

On July 2, 2013, the Obama administration declared that it was delaying the effective date of the Patient Protection and Affordable Care Act’s Employer Mandate until January 1, 2015. The Employer Mandate, which was scheduled to become effective on January 1, 2014, required all large employers to offer health care coverage to their full-time employees or pay a penalty. Most importantly, this delay means that the penalties to large employers for failure to provide health insurance coverage will not be enforced for another year. You may read the full statement issued by the U.S. Department of Treasury here.

A key component of the Patient Protection and Affordable Care Act ("PPACA") involves expanding Medicaid to anyone who earns up to 133 percent of the poverty level. In its landmark ruling last year the Supreme Court, while upholding PPACA, ruled that states could not be compelled to expand the joint federal-state Medicaid program.

State legislatures and governors across the country have considered whether to expand Medicaid, with only 23 states and the District of Columbia implementing an expansion according to the (We have identified that the following link is no longer active, and it has been removed.) Under the PPACA, 100 percent of the cost of the Medicaid expansion will be covered by the federal government from 2014 through 2016. The federal government's contribution will gradually decline until reaching 90 percent in 2022 and beyond.

On Tuesday, June 11, members of the House Committee on Energy and Commerce sent a letter to acting IRS Commissioner Daniel Werfel requesting information regarding how the IRS handles confidential medical information. The letter comes after a recent lawsuit alleging that the IRS illegally seized over 60 million medical records in 2011.

On Tuesday, June 11, members of the House Committee on Energy and Commerce sent a letter to acting IRS Commissioner Daniel Werfel requesting information regarding how the IRS handles confidential medical information. The letter comes after a recent lawsuit alleging that the IRS illegally seized over 60 million medical records in 2011.

The lawsuit, a class action filed by an unnamed health care provider against 15 unnamed IRS agents, alleges that the agents improperly seized the medical records in violation of the Fourth Amendment during a search executed on March 11, 2011. According to the complaint, the agents seized more than ten million medical records despite knowing that the records were not within the scope of their warrant, (which authorized only the seizure of financial records related to a former employee). The seized records allegedly contained "intimate and private information . . . including psychological counseling, gynecological counseling, [and] sexual or drug treatment." The complaint further alleges that the agents threated to "rip out" the servers containing the medical data if the company's IT personnel did not voluntarily transfer the information to the IRS.

The Treasury Department and IRS continue to roll out new regulations related to the implementation of the Patient Protection and Affordable Care Act ("PPACA"). On May 10, 2013, the Treasury Department and IRS released the draft regulations, "Computation of, and Rules Relating to, Medical Loss Ratio", which are intended to help Blue Cross and Blue Shield ("BCBS") organizations comply with the Medical Loss Ratio (“MLR”) rules created by the PPACA.

The Treasury Department and IRS continue to roll out new regulations related to the implementation of the Patient Protection and Affordable Care Act ("PPACA"). On May 10, 2013, the Treasury Department and IRS released the draft regulations, "Computation of, and Rules Relating to, Medical Loss Ratio", which are intended to help Blue Cross and Blue Shield ("BCBS") organizations comply with the Medical Loss Ratio (“MLR”) rules created by the PPACA.

While many thought the Blue Cross Blue Shield of Michigan ("BCBSM") conversion bills would be signed into law at the end of 2012, it was not until March 18, 2013 that Governor Snyder signed the proposed legislation into law. The BCBSM conversion bills convert BCBSM from "a tax exempt charitable and benevolent institution" into a nonprofit mutual health insurance company. BCBSM has been operating as a tax-exempt nonprofit since Public Act 350 was signed into law in 1980. (This Public Act is referred to as the previous BCBSM statute.) The previous BCBSM statute made BCBSM Michigan’s “insurer of last resort,” requiring it to accept all customers regardless of their health.

While many thought the Blue Cross Blue Shield of Michigan ("BCBSM") conversion bills would be signed into law at the end of 2012, it was not until March 18, 2013 that Governor Snyder signed the proposed legislation into law. The BCBSM conversion bills convert BCBSM from "a tax exempt charitable and benevolent institution" into a nonprofit mutual health insurance company. BCBSM has been operating as a tax-exempt nonprofit since Public Act 350 was signed into law in 1980. (This Public Act is referred to as the previous BCBSM statute.) The previous BCBSM statute made BCBSM Michigan’s “insurer of last resort,” requiring it to accept all customers regardless of their health.

On March 7 and 8, 2013, the members of Foster Swift’s Health Care Law Group attended the 19th Annual Health Law Institute. This two-day institute, which is co-sponsored by the Institute for Continuing Legal Education and the Health Care Law Section of the State Bar of Michigan, focused on recent legal developments in health care law. Specific topics addressed at this year’s Health Law Institute included:

On March 7 and 8, 2013, the members of Foster Swift’s Health Care Law Group attended the 19th Annual Health Law Institute. This two-day institute, which is co-sponsored by the Institute for Continuing Legal Education and the Health Care Law Section of the State Bar of Michigan, focused on recent legal developments in health care law. Specific topics addressed at this year’s Health Law Institute included:

On January 30, 2013, the Departments of Treasury, Labor, and Health and Human Services (collectively, the “Departments”) jointly released proposed rules related to the coverage of preventive services under the Patient Protection and Affordable Care Act (“PPACA”). When initially enacted, PPACA required certain health plans to provide benefits for particular preventive health services, including coverage of contraceptives, without the imposition of cost sharing measures (i.e., individuals covered by the plan would not be required to pay anything for the services). This coverage requirement became effective on the first day of the plan year that followed August 1, 2012. For calendar year plans, the effective date was January 1, 2013.

On January 30, 2013, the Departments of Treasury, Labor, and Health and Human Services (collectively, the “Departments”) jointly released proposed rules related to the coverage of preventive services under the Patient Protection and Affordable Care Act (“PPACA”). When initially enacted, PPACA required certain health plans to provide benefits for particular preventive health services, including coverage of contraceptives, without the imposition of cost sharing measures (i.e., individuals covered by the plan would not be required to pay anything for the services). This coverage requirement became effective on the first day of the plan year that followed August 1, 2012. For calendar year plans, the effective date was January 1, 2013.

On February 11, 2013, the Departments of Justice and Health and Human Services jointly released a report stating that the government recovered $4.2 billion in fiscal year 2012 and for every dollar spent on health care-related fraud and abuse investigations in the last three years, the government recovered $7.90. The report indicates that this is the highest 3-year average return on investment in the 16 year history of the Health Care Fraud and Abuse program. The Health Care Fraud Prevention and Enforcement Action Team (“HEAT”), which has operations in Detroit, was instrumental in this recovery effort.

Governor Rick Snyder announced that his 2014 budget includes support for the expansion of Medicaid eligibility to Michigan residents without insurance. Speaking at a press conference in Lansing on Wednesday, February 6th, Governor Snyder said expansion would save costs, increase care, and help businesses.

Governor Rick Snyder announced that his 2014 budget includes support for the expansion of Medicaid eligibility to Michigan residents without insurance. Speaking at a press conference in Lansing on Wednesday, February 6th, Governor Snyder said expansion would save costs, increase care, and help businesses.

As previously discussed, the Patient Protection and Affordable Care Act requires employers to provide notice to their employees related to Health Insurance Exchanges (the “Notice”). The specifics concerning the Notice may be found here. The Notice was required to be given to each current employee not later than March 1, 2013.

As previously discussed, the Patient Protection and Affordable Care Act requires employers to provide notice to their employees related to Health Insurance Exchanges (the “Notice”). The specifics concerning the Notice may be found here. The Notice was required to be given to each current employee not later than March 1, 2013.

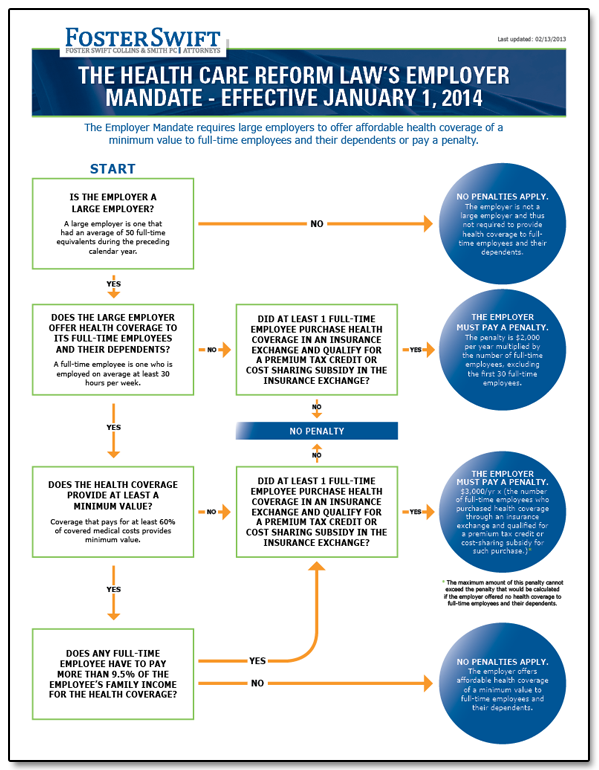

Employers with 50 or more full time equivalent employees (“FTEs”) will be subject to a penalty tax for: (1) failing to offer health care coverage to all full time employees; ( 2) offering minimum essential coverage that is unaffordable; or (3) offering minimum essential coverage where the Plan pays less than 60% of cost. This is often referred to as the Employer Mandate of PPACA.

Employers with 50 or more full time equivalent employees (“FTEs”) will be subject to a penalty tax for: (1) failing to offer health care coverage to all full time employees; ( 2) offering minimum essential coverage that is unaffordable; or (3) offering minimum essential coverage where the Plan pays less than 60% of cost. This is often referred to as the Employer Mandate of PPACA.

The Patient Protection and Affordable Care Act ("PPACA") requires "large employers" to provide affordable health coverage of a minimum value to full-time employees and their dependents starting in 2014. A large employer failing to do so may be subject to penalties.

The Patient Protection and Affordable Care Act ("PPACA") requires "large employers" to provide affordable health coverage of a minimum value to full-time employees and their dependents starting in 2014. A large employer failing to do so may be subject to penalties.

Coverage is considered affordable to an employee if the employee portion of the self-only premium for the employer's lowest-cost coverage does not exceed 9.5% of the employee's household income, but only if the lowest-cost coverage provides a minimum value.

Over the past several weeks, the nation has seen a flurry of announcements issued by states as to how such states will implement and operate the health insurance exchanges (“HIE”) required by the Affordable Care Act. States have three options as to how they may run their HIEs:

On Monday, November 26, 2012 the Department of Health and Human Services ("DHHS") issued proposed rules on: (1) standards related to essential health benefits, actuarial value and accreditation, and (2) health insurance market rules and rate review. The Department of Treasury, the Department of Labor, and DHHS issued combined proposed rules for the incentives of wellness programs. Comments on these proposals must be received no later than December 26, 2012. So those interested in commenting have a short window to examine the three sets of rules. For more on these topics and how they will impact you, stay tuned to the Foster Swift Health Care Blog.

As we previously reported, the Department of Health & Human Services (“DHHS”) extended some important deadlines for states establishing State-Based Insurance Exchanges or State Partnership Exchanges for 2014. Specifically, DHHS extended the submission deadline for State-Based Exchange Blueprints to December 14, 2012. However, the administration previously still required states to submit Declaration Letters of their intent to build state-based Health Insurance Exchanges by November 16th. However, as of Thursday (November 15th), only 17 states and the District of Columbia had committed to building their own Exchanges. This is far fewer than envisioned by the Obama administration when the law was passed in 2010. To give states more time, the Obama administration extended the deadline for the Declaration letters until December 14th. Thus, both Blue Prints of the specifics of the Exchange and Declaration Letters of states wishing to run their own Exchange are due on December 14th.

Last Friday, the U.S. Department of Health & Human Services ("DHHS") extended important deadlines related to those states desiring to establish State-Based Insurance Exchanges or State Partnership Exchanges for 2014. Specifically, Kathleen Sebelius, Secretary of DHHS, advised governors that DHHS had extended certain deadlines related to the submission of Declaration Letters and Blueprints, stating that DHHS is committed to providing states with flexibility for building a marketplace that meet each state's needs.

Last Friday, the U.S. Department of Health & Human Services ("DHHS") extended important deadlines related to those states desiring to establish State-Based Insurance Exchanges or State Partnership Exchanges for 2014. Specifically, Kathleen Sebelius, Secretary of DHHS, advised governors that DHHS had extended certain deadlines related to the submission of Declaration Letters and Blueprints, stating that DHHS is committed to providing states with flexibility for building a marketplace that meet each state's needs.

As President Obama moves into his second term, health care reform moves forward with him. Wholesale repeal of the Patient Protection and Affordable Care Act (PPACA) now seems highly unlikely. With the majority of the PPACA provisions slated to go into effect in 2014, employers need to be ready.

Foster Swift has developed guides to aid employers with their preparation efforts. Click the links below to download these guides.

|

EMPLOYER & INDIVIDUAL

|

PPACA PROVISION

|

Documents updated 07-12-2013

If you have any questions regarding health care reform, please contact a member of the Foster Swift Health Care Law Group.

On October 11, 2012, the Lansing Regional Chamber of Commerce hosted its annual Healthcare Forum. A half-day event, the Healthcare Forum brings together mid-Michigan leaders in the health care industry to provide updates on the latest issues. This year’s forum, titled “Countdown to 2014 – The Tools to Conform to Healthcare Reform,” drew nearly 100 attendees and featured topics including:

At the end of August, Governor Rick Snyder announced that Michigan will be pursuing a federal-state partnership for its health insurance exchange. Health insurance exchanges are a requirement of the federal Health Care Reform law. Health insurance exchanges are designed to facilitate the purchase of health insurance by consumers through an online, cost-competitive forum. Each state has the option to: (1) operate its own health insurance exchange; (2) partner with the federal government; or (3) allow the federal government to manage its health insurance exchange.

At the end of August, Governor Rick Snyder announced that Michigan will be pursuing a federal-state partnership for its health insurance exchange. Health insurance exchanges are a requirement of the federal Health Care Reform law. Health insurance exchanges are designed to facilitate the purchase of health insurance by consumers through an online, cost-competitive forum. Each state has the option to: (1) operate its own health insurance exchange; (2) partner with the federal government; or (3) allow the federal government to manage its health insurance exchange.

Foster Swift lawyers were well represented at the Annual Meeting of the State Bar of Michigan's Health Care Law Section held on September 19th. Gilbert Frimet, Gary McRay, Jennifer Kildea Dewane, and Nicole Stratton, members of Foster Swift Health Care Law Practice Group, all traveled to Detroit to attend the meeting.

With the United States Supreme Court having ruled that nearly all of the provisions in the Patient Protection and Affordable Care Act (“PPACA”) are constitutional, employers are legally obligated to comply with PPACA's requirements. One such requirement of particular interest to employers is the employee health insurance exchange notice requirement.

Foster Swift health care law attorney, Johanna Novak, was recently interviewed on Michigan Business Network radio concerning the United States Supreme Court's long-anticipated decision on the Patient Protection and Affordable Care Act (the "Act"). The interview aired on July 6, 2012, and was separated into two parts. Podcasts for both parts of Johanna's interview can be accessed here.

Foster Swift health care law attorney, Johanna Novak, was recently interviewed on Michigan Business Network radio concerning the United States Supreme Court's long-anticipated decision on the Patient Protection and Affordable Care Act (the "Act"). The interview aired on July 6, 2012, and was separated into two parts. Podcasts for both parts of Johanna's interview can be accessed here.

Today, the United States Supreme Court released its highly anticipated opinion regarding the constitutional challenges to the Patient Protection and Affordable Care Act (the "Act"). The Court ultimately concluded that the Act was constitutional, but it did not grant a complete victory to the government. The Court also held that the federal government may not withhold all Medicaid funds from States that fail to comply with the expansion of Medicaid provisions of the Act. Instead, the federal government may only withhold new Medicaid funds from States that do not comply.

In late 2011, the Supreme Court of the United States announced that it would take up four issues regarding the Patient Protection and Affordable Care Act ("PPACA"). The Court is expected to hear oral arguments in late March of 2012 and provide a decision in June of 2012.

Three of the four issues to be reviewed by the Court center around PPACA's Individual Mandate. The Individual Mandate (also known as the minimum coverage provision) requires that, beginning in 2014, individuals who fail to maintain a minimum level of health insurance coverage for themselves and their dependents pay a penalty, calculated in part on the basis of the individual's household income as reported on the individual's federal income tax return. This is likely the most controversial provision of PPACA.

The four issues to be considered by the Court are as follows:

If you are already a subscriber to Foster Swift's health care law blog, you might be interested in Foster Swift's Health Care Law E-News as well. These newsletters provide an in-depth discussion on specific issues that are of interest to those in the health care industry. See what the latest Health Care Law E-News has to offer.

If you are already a subscriber to Foster Swift's health care law blog, you might be interested in Foster Swift's Health Care Law E-News as well. These newsletters provide an in-depth discussion on specific issues that are of interest to those in the health care industry. See what the latest Health Care Law E-News has to offer.

![]() On Wednesday, February 2nd, the U.S. House of Representatives approved a measure to repeal the CLASS Act. A similar repeal measure is pending in the U.S. Senate.

On Wednesday, February 2nd, the U.S. House of Representatives approved a measure to repeal the CLASS Act. A similar repeal measure is pending in the U.S. Senate.